DOWNLOAD SEKARANG

BOLA86 - LOGIN BERMAIN FAVORIT ONLINE TERBESAR

bola86 adalah tempat nonton laga piala atau platform bermain yang semuanya gratis tanpa biaya apapun yang membuat nobar semakin seru bersama teman

link login dan tempat nobar.

BOLA86 login link terbaru ini lebih dikenal sebagai server game favorit mpo platform tempat taruhan bola mix-parlay sportsbook online resmi terpercaya. Kebanyakan orang-orang yang berlangganan di situs game online gampang menang bola86 adalah orang-orang yang sedang mencari kenyamanan dan pengalaman bermain yang baik di indonesia, kenyamanan bermain tentu didapatkan keterampilan pelayanan customer service dan juga kemudahan dalam melakukan game game online di situs bola86, kedua hal tersebut sudah cukup dalam memberikan pengalaman bermain yang baik kepada pemain, oleh karena itulah sangat penting sekali bagi para pemain untuk berlangganan bersama situs game online gampang menang hari ini, sebab dengan begitu maka kenyamanan serta kemenangan akan sangat mudah untuk didapatkan.

Keunggulan Berlangganan Di Game Game Online Gampang Menang Hari Ini

Sebelum memutuskan untuk berlangganan bersama situs game online online gampang menang hari ini yaitu bola86, ada baiknya pengguna mempelajari terlebih dahulu beberapa keunggulan dari layanan game game online hari ini bola86 ini.

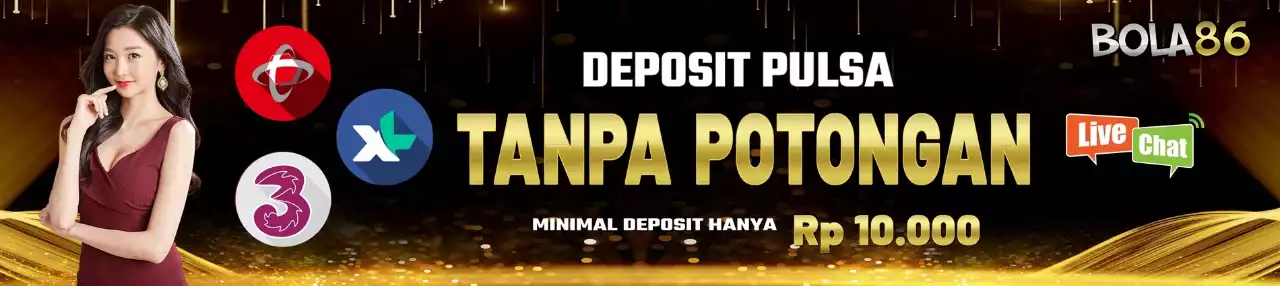

- situs game online bola86, maka kelengkapan metode top up saldo akan didapatkan dengan mudah, untuk metode top up saldo di situs bola86 sendiri ada : metode top up saldo menggunakan bank, e-wallet dan pulsa. setelah itu juga memiliki metode top up saldo bantu dalam bermain permainannya.

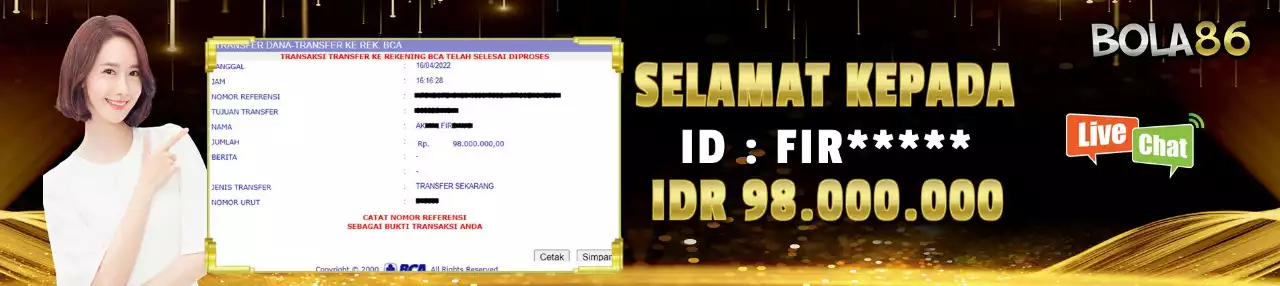

- menyediakan layanan pelangganan professional selama 24 jam dalam sehari : bola86 merekrut layanan pelanggan professional yang berpengalaman dalam melayani para pengguna game online di indonesia, dengan begitu maka, banyak member pasti dijamin tentu mendapatkan kepuasan dalam konteks "pelayanan memuaskan" setiap saat nya. Untuk proses lamanya top up saldo serta penarikan juga tidak membutuhkan waktu yang lama, sehingga para pengguna bisa menikmati layanan ini setiap saat.

- Dengan memiliki akses ke dalam berbagai macam game terbaik terbaru, tentu akan meningkatkan pengalaman bermain para pemain itu sendiri, kemudian para pemain juga akan mendapatkan informasi mengenai permainan baru dan terbaik lebih awal di situs game online bola86 dibandingkan dari situs game dengan permainan yang tidak lengkap.

- promo minimal top up saldo paling termurah : pastinya beberapa situs game online membuatkan minimal dp yang lumayan tinggi terasa di kantong kepada pemain, dengan ini memancing situs nonton online gampang menang seperti situs bola86 untuk menawarkan minimal top up saldo termurah untuk dinikmati oleh seluruh pengguna di indonesia, harga top up saldo termurah yang ditawarkan adalah berkisar 10 ribu rupiah dengan minimal penarikan sebesar 50 ribu rupiah.

Bola86 Situs Game Online Hari Ini Dan Game Online Gampang Menang Terbaik

Bola86 adalah situs game online hari ini online gampang menang menyediakan berbagai daftar link game online game terbaik indonesia win rate tinggi. Selamat datang di situs game online hari ini di indonesia yaitu di situs bola86, website game online hari ini telah membuktikan dirinya telah memberikan segelintir pemain kemenangan yang sensational hingga setiap harinya. Situs bola86 sendiri telah sukses memperkenalkan berbagai macam produk game online terbaiknya terhadap masyarakat di indonesia, sehingga apabila diperhatikan banyak sekali pengguna-pengguna baru berdatangan untuk mendaftarkan dirinya di situs game online online ini. Visi dan misi dari situs game online ini juga adalah untuk memberikan pengalaman bermain terbaik serta memuaskan keinginan para pengguna dalam mendapatkan kemenangan di game game online hari ini, maka dari itulah situs bola86 sendiri setiap harinya akan memberikan informasi seputar game-game game unggulan dan terbaik agar bisa dinikmati oleh seluruh pengguna setiap harinya.